CoreWeave, Inc. (CRWV)

CoreWeave: Bargain In The Rubble

CoreWeave reported Q4 results and FY26 outlook on Thursday after the bell, dragging the stock down as much as 21% on Friday trading. Management is guiding FY26 to the $12B-$13B range, versus estimates closer to $12B, and reported a jump in backlog from $55.6B to $66.8B. CapEx guidance surged, as well, to $30B–$35B, more than double the $14.9B spent in FY25, and net losses widened, again.

More Downside For CoreWeave Stock?

CoreWeave stock dropped 19% on Friday to $79.56 and has continued to slide another 4% in pre-market trading. This sharp Friday decline was primarily triggered by a broader sell-off in the AI infrastructure sector and investor concerns regarding sustainable capital expenditure levels among major cloud providers.

CoreWeave: Focus On Prospects, Not Growing Pains

CoreWeave reported strong revenue growth but missed margin and income targets, leading to a sharp stock selloff. The AI cloud company is experiencing significant growing pains as it rapidly scales to meet hyperscaler demand, adding ~260 MW of new power in Q4. The market is concerned about low margins and high-interest expenses from substantial borrowing to fund AI GPU data center expansion.

Investors Hated CoreWeave's Earnings. It Might Be Even Worse Than They Realize

Artificial intelligence (AI)-focused cloud infrastructure provider CoreWeave ( NASDAQ:CRWV ) released its fourth quarter earnings on Thursday, and the market's reaction was swift and brutal.

CoreWeave: Another CapEx Tantrum

CoreWeave, Inc. delivered 110% Y/Y revenue growth and a 342% Y/Y backlog increase, driven by surging GPU compute demand and major OpenAI contracts. Despite a 9% post-earnings sell-off over CapEx and profitability concerns, I view CRWV's preferred Nvidia partnership and aggressive CapEx as key competitive advantages. Surge in interest expenses and $30-35B CapEx guidance are raising profitability concerns for CoreWeave in the short term. However, the long term growth run-way is promising as industry CapEx soars.

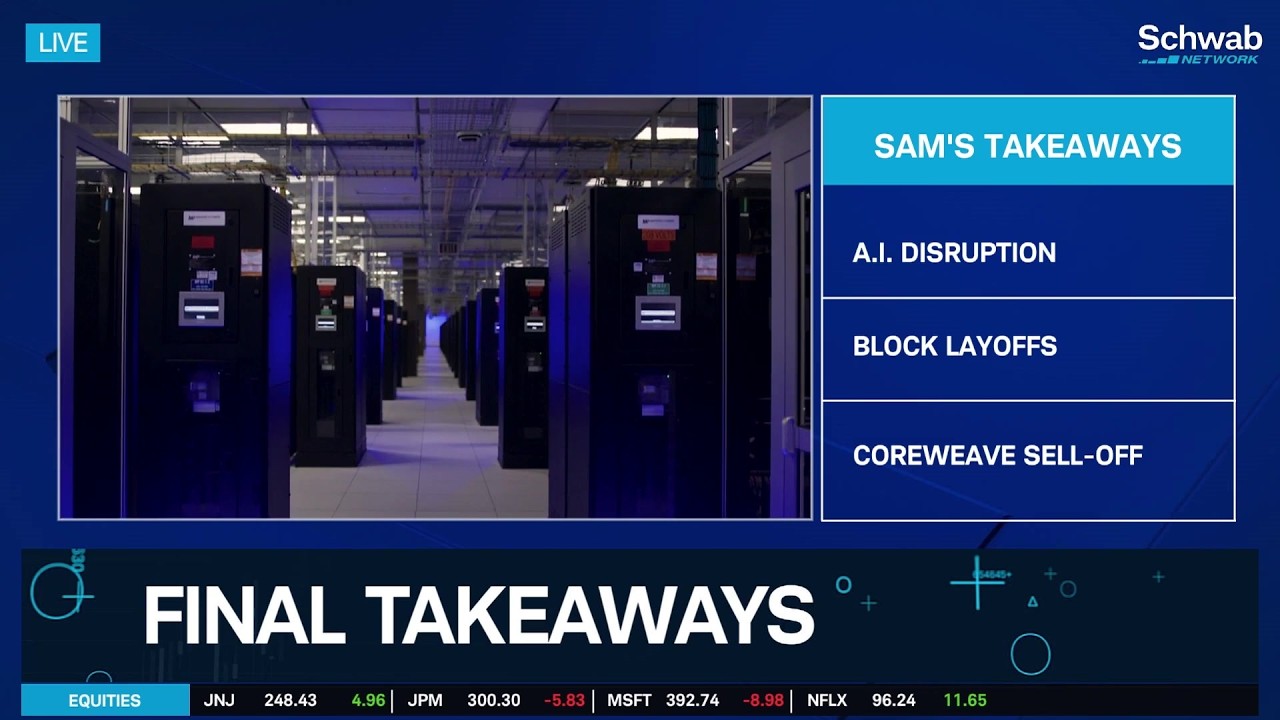

Friday's Final Takeaways: Two Sides of AI Disruption in CRWV & XYZ

Sam Vadas talks about her final market takeaways to close a volatile week for tech on Wall Street. Among her top headlines: the widespread layoffs at Block (XYZ) and CoreWeave's (CRWV) strong selling action after earnings.

Spending Fears Weigh on CoreWeave, But the Backlog Tells Another Story

CoreWeave NASDAQ: CRWV stock is depressed in Q1 2026 due to concerns about spending, dilution, and execution risks. However, analyst sentiment, institutional trends, results, and the backlog suggest those fears may be overblown.

CoreWeave: From Growth Story To Capital Story

CoreWeave, Inc. delivered $1.57B in Q4 revenue, up 110% YoY, with backlog expanding to $66.8B and FY revenue reaching $5.13B. CRWV management guided 2026 revenue to $12–$13B while committing to $30–$35B of CapEx, reframing the narrative toward capital discipline. Adjusted EBITDA reached $898M (57% margin), but the Q4 GAAP loss widened to $452M as interest expense surged to $388M.

Nvidia-Backed CoreWeave's Stock Plunges on Weak Forecast, Even as Its AI Backlog Grows

Nvidia-backed CoreWeave's stock could be set to lose a fifth of its value in just one session.

CoreWeave CEO defends spending plans, tries to combat debt narrative as stock plummets nearly 20%

Coreweave's stock plummeted on disappointing revenue guidance and a higher-than-expected capital expenditures forecast. CEO Mike Intrator addressed concerns about CoreWeave spending, saying the company has intentionally accelerated its infrastructure buildout to meet demand.

CoreWeave shares plunge after Q4 losses, revenue outlook misses estimates

CoreWeave Inc. (NASDAQ: CRWV) shares tumbled 17.6% on Friday after the cloud computing company reported wider-than-expected fourth-quarter losses and provided a cautious revenue forecast for the first quarter. The company posted Q4 revenue of $1.572 billion, slightly above Wall Street expectations of $1.55 billion.

CoreWeave: Shades of Amazon's Growth-First Strategy

Thursday, CoreWeave ( CRWV ) reported Q4 earnings results after the market close. The large-scale GPU-accelerated operator reached an impressive milestone, becoming the fastest cloud provider to reach $5 billion in annual revenue.