Advanced Micro Devices, Inc. (AMD)

5 Things to Know Before the Stock Market Opens on Thursday

Stock futures are lower as worries about AI spending pressure big tech shares; Tesla shares are falling after the electric vehicle maker said rising R&D costs squeezed profits; Alphabet shares are taking a hit too after the company lifted its capital expenditures forecast; strong AI spending trends could favor chipmaker Intel, due to release results after the closing bell today; and Advanced Micro Devices is set to showcase its latest tech at its “Advancing AI” keynote. Here's what you need to know today.

AMD expected to launch next generation of AI infrastructure to challenge Nvidia

Advanced Micro Devices is set to launch a raft of AI hardware that will rival Nvidia on Thursday at an event at a downtown convention center in San Francisco.

AMD: The Full-Stack AI Opportunity

AMD (AMD) remains a compelling buy, with a new base case price target of $671 (21% upside) and a bullish scenario at $807.87 (45% upside). AMD's flexible, customizable AI infrastructure—spanning GPUs, CPUs, DPUs, networking, and rack-scale systems—positions it as a strong alternative to Nvidia, especially for hyperscalers seeking to avoid vendor lock-in. Rising analyst expectations reflect robust AI-driven growth: Q2 revenue consensus at $11.3B (+47% YoY), EPS at $1.61 (+235% YoY), and EBITDA/fcf estimates up 22–28%.

The AI Bull Case Lives On: What You Need to Know

While recent pullbacks in AI stocks have concerned investors, the underlying fundamentals of the AI revolution tell a vastly different narrative.

AMD's Microsoft Win Signals Dominance Over NVIDIA and Our Price Target Reflects It

The AI infrastructure story at Advanced Micro Devices (NASDAQ:AMD | AMD Price Prediction) keeps compounding.

AMD Just Landed a $5 Billion AI Coup — Is Nvidia's Grip Finally Starting to Slip?

Artificial intelligence spending continues to redraw the competitive landscape across the technology sector.

AMD is investing $5 billion into Anthropic as it seeks to cut into Nvidia's dominance

The two companies also struck a chip deal.

How AMD Captures Significant Market Share From Nvidia

AMD (NASDAQ: AMD | AMD Price Prediction) and NVIDIA (NASDAQ: NVDA) both closed spring reporting periods with blockbuster AI numbers, but the businesses are pulling in different directions.

AMD, Anthropic announce strategic AI infrastructure partnership with up to $5B investment

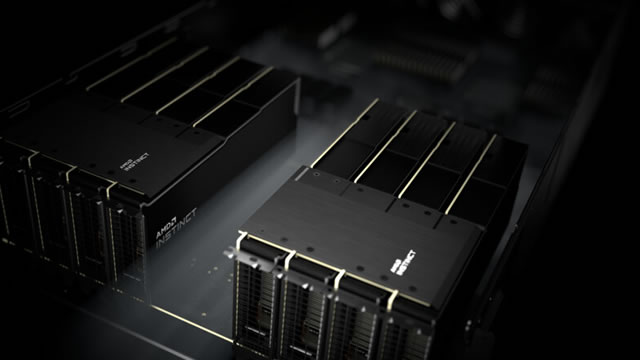

Advanced Micro Devices Inc (NASDAQ:AMD, XETRA:AMD) and Anthropic announced a strategic partnership on Wednesday that includes the deployment of up to 2 gigawatts of AMD's upcoming Instinct MI450 Series GPUs, a multi-year engineering collaboration, and a planned equity investment by AMD of up to $5 billion in the artificial intelligence startup. Under the agreement, Anthropic plans to deploy up to 2 gigawatts of AMD Helios rack-scale solutions, with the first gigawatt expected to begin deployment in the first half of 2027.

Is Most-Watched Stock Advanced Micro Devices, Inc. (AMD) Worth Betting on Now?

Recently, Zacks.com users have been paying close attention to Advanced Micro (AMD). This makes it worthwhile to examine what the stock has in store.

Looking for Stocks with Positive Earnings Momentum? Check Out These 2 Computer and Technology Names

Investors looking for ways to find stocks that are set to beat quarterly earnings estimates should check out the Zacks Earnings ESP.

AMD to invest up to $5 billion in Anthropic as part of computing power deal

AMD announced a partnership with Anthropic and said it will invest up to $5 billion in the AI company. As part of the deal, Anthropic will deploy 2 gigawatts of the AMD Instinct MI450 Series GPUs in AMD Helios rack-scale solutions.