Merck & Co., Inc. (MRK)

Merck & Co., Inc. (MRK) is Attracting Investor Attention: Here is What You Should Know

Recently, Zacks.com users have been paying close attention to Merck (MRK). This makes it worthwhile to examine what the stock has in store.

Merck: Keytruda Remains Resilient Despite LOE Risks - Buy Upon Correction

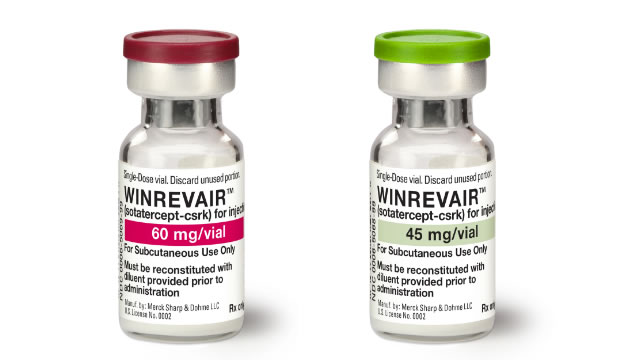

New KEYTRUDA indications are expected to preserve Merck's top line, significantly aided by the high single-digit Animal Health/Livestock and the triple-digit Winrevair revenue growth in FY2025. KEYTRUDA QLEX, with the expected ~20Y monopoly on injection delivery and the projected ~40% user transition by 2027, is positioned to bridge revenue risks after the original KEYTRUDA's 2028 LOE. MRK's healthier balance sheet, secure dividends, and disciplined capital allocation support resilience, despite the lumpy intermediate-term adjusted EPS prospects.

Merck: The Spike Doesn't Make It Overvalued

Merck has surged more than 50% in six months, underpinned by a robust asset portfolio and strong shareholder return strategy. Keytruda, MRK's top-selling drug, faces a 2028 patent cliff, but ongoing innovation and new approvals like Qlex aim to mitigate revenue risk. Despite Gardasil's recent sales decline, MRK's vaccine portfolio remains resilient, with Capvaxive sales up 460% to more than $1 billion annualized.

Merck: A Buy For 2026, But The Clock Is Still Ticking

Merck is rated Buy after extending Keytruda's patent protection to late-2029, delaying the anticipated patent cliff, and unlocking significant near-term value. The extended exclusivity creates a one-time cash windfall and enables deeper penetration of Keytruda QLEX, potentially adding $10/share in 'hidden alpha.' MRK's 40:30:30 strategy—QLEX migration, pipeline execution, and business development—offers a realistic path to offset Keytruda's eventual decline.

From Bargain To Balancing Act: Merck's Next Test Begins (Rating Downgrade)

Merck & Co. is no longer a deep-value patent cliff trade but a fairly valued defensive compounder. Future returns now depend on execution and pipeline delivery, not multiple expansion. Keytruda erosion may be slower than feared for MRK, but LOE still creates a major revenue hole. Extended growth helps, yet replacement needs to accelerate meaningfully. New products and the Prometheus Biosciences pipeline show promise but remain early-stage revenue streams. Several more quarters of scaling are needed before confidence in gap-filling is justified.

Merck: Pipeline Building Despite The Light FY26 Guide, Major Momentum

Merck delivered a strong Q4 double beat, with robust pipeline momentum and a healthy new launch cycle supporting a continued buy rating. MRK raised its price target to $130, reflecting normalized $10 EPS and a 13x P/E multiple, still below peers despite Keytruda LOE risks. Keytruda, Ohtuvayre, and Winrevair drive growth, while 80+ Phase 3 studies and recent acquisitions strengthen the pipeline and long-term outlook.

Merck's Subdued 2026 Outlook: What it Means After Q4 Results?

MRK posts conservative 2026 sales and EPS outlook, given acquisition charges. Keytruda, Animal Health and new drug launches are expected to drive 2026 growth.

Merck & Co., Inc. (MRK) Q4 2025 Earnings Call Transcript

Merck & Co., Inc. (MRK) Q4 2025 Earnings Call Transcript

MRK Q4 Earnings & Sales Beat Estimates, Stock Down on Weak '26 View

Merck tops Q4 EPS and sales estimates as Keytruda drives growth, but shares fall in pre-market trading as 2026 guidance disappoints.

Merck (MRK) Reports Q4 Earnings: What Key Metrics Have to Say

Although the revenue and EPS for Merck (MRK) give a sense of how its business performed in the quarter ended December 2025, it might be worth considering how some key metrics compare with Wall Street estimates and the year-ago numbers.

Merck shares dip as 2026 outlook misses Wall Street expectations

Merck & Co Inc (NYSE:MRK, XETRA:6MK) shares fell 2% at Tuesday's opening bell after the drugmaker issued a 2026 outlook that came in below Wall Street expectations, overshadowing a fourth-quarter earnings and revenue beat. Merck forecast 2026 revenue of $65.5 billion to $67.0 billion, compared with analysts' estimates of $67.6 billion, and adjusted earnings of $5 to $5.15 per share versus expectations of $5.36.

Merck (MRK) Q4 Earnings and Revenues Beat Estimates

Merck (MRK) came out with quarterly earnings of $2.04 per share, beating the Zacks Consensus Estimate of $2.03 per share. This compares to earnings of $1.72 per share a year ago.