CVS Health Corporation (CVS)

CVS Stock Soars 47% YTD: Is Digital Growth Fueling a Buy Opportunity?

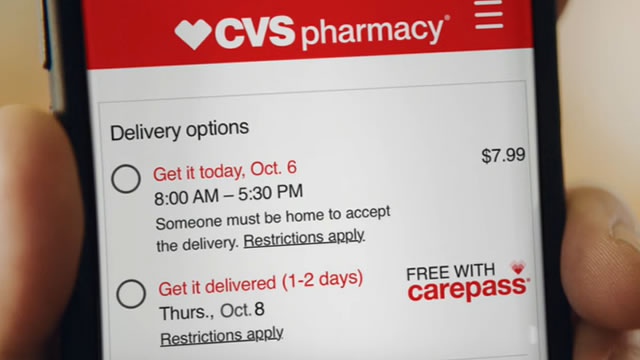

CVS Health is consistently increasing investments in fast-growing spaces like enterprise data platforms, cloud capabilities and digital products.

CVS opens smaller format stores as industry sees big shift

CVS is opening new stores around the nation, but they will be significantly smaller and focus only on pharmacy services. The move comes as the industry undergoes a major shift.

CVS is opening smaller drugstores that only have pharmacies

CVS said it will open a dozen or more drugstores that only have pharmacies as it scrambles to remain competitive against rivals like Target, Amazon, Walgreens, and Rite Aid. The smaller stores, each location averaging less than 5,000 square feet, will feature a full service pharmacy with limited over-the-counter products for purchase.

CVS Plans Chain of Smaller-Footprint Pharmacy-Focused Stores

CVS is reportedly opening 12 smaller-footprint locations focused more on healthcare than consumer products. As The Wall Street Journal (WSJ) reported Sunday (March 9), the new stores will feature full-service pharmacies but limited retail.

Has CVS Health Stock Turned Things Around?

Last year, shares of healthcare company CVS Health (CVS 1.92%) crashed by more than 43%. The company struggled with rising medical costs and routinely missed earnings expectations.

The Smartest Dividend Stocks to Buy With $3,000 Right Now

So you've got $3,000 -- or perhaps just $300 or maybe $30,000 -- to invest and you want to park that money in dividend-paying stocks as you've paid off all your high-interest debt, have plumped up your emergency savings, and won't need the money for anything in the near or medium term. That's very smart of you!

Is Trending Stock CVS Health Corporation (CVS) a Buy Now?

Zacks.com users have recently been watching CVS Health (CVS) quite a bit. Thus, it is worth knowing the facts that could determine the stock's prospects.

CVS cuts bonuses after low profit levels in 2024

CVS Health said on Friday it has cut bonuses for some employees because of its low profit levels last year, as the healthcare conglomerate grapples with higher costs across its Medicare plans.

This stock is up 50% already since Jim Cramer's warning

Jim Cramer, the eccentric host of ‘Mad Money' on CNBC, is one of the most recognizable voices covering finance in the United States. Recognizable, however, does not necessarily equate to reverence.

Top 2 cheap stocks to buy for 2025

The US consumer price index (CPI) was up more than expected in January, raising doubts about the Federal Reserve's ability to lower interest rates further in 2025.

CVS Health: One Good Quarter Is Not Enough; Retain Sell

Despite a recent 45% rally, I maintain a 'Sell' view on CVS due to its underwhelming execution record and rising leverage levels. CVS' Q4 results showed a surprising EBIT margin beat, but continued margin erosion in its insurance business remains a concern. Improved margin performance in FY25 is possible with better insurance policy terms and reduced loss-making membership counts but given a poor execution record, it is better to wait for evidence.

Is It Too Late to Buy CVS Health Stock for the High-Yield Dividend?

After underperforming throughout 2024, shares of CVS Health (CVS -0.81%) are surging. From the end of 2024 through Feb. 14, the stock climbed 46.7% higher.