Rebalancing is rarely the most exciting topic in investing circles. It doesn’t generate headlines or spark debates like stock picking or market timing. Yet, for those committed to long-term investing success, rebalancing is one of the quiet disciplines that can make all the difference between a portfolio that survives and one that thrives.

Understanding the Role of Rebalancing

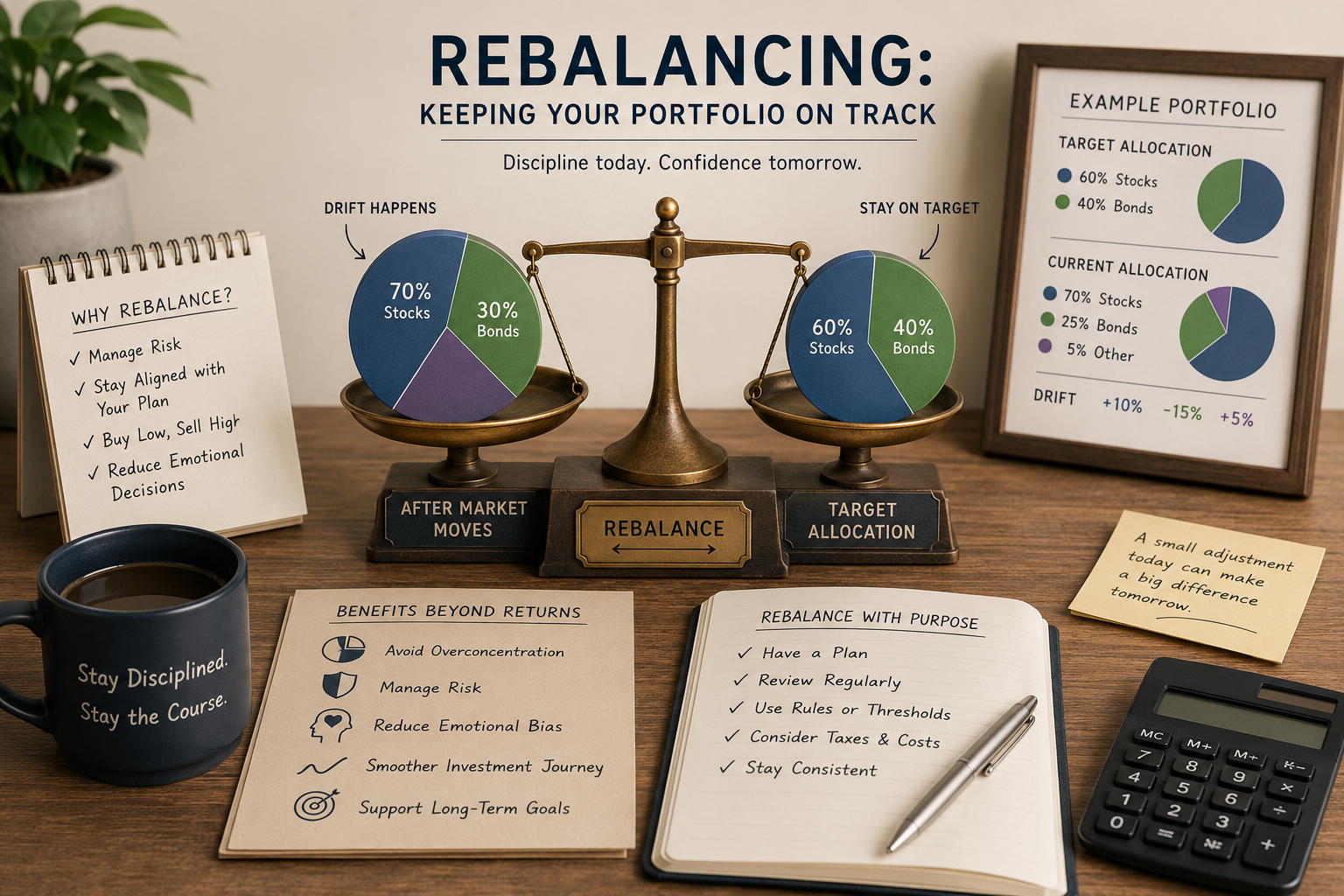

At its core, rebalancing is the process of realigning your portfolio’s asset allocation back to its original targets. Over time, as markets move, certain assets will outperform while others lag. Left unchecked, this drift can expose you to unintended risks and potentially undermine your investment goals. For example, a portfolio that started as 60% stocks and 40% bonds may morph into 70% stocks after a strong bull market—leaving you more exposed to equity risk than you intended.

Why Discipline Matters

It’s easy to let winners run and put off trimming back. But the discipline to periodically rebalance—selling some of what’s done well and buying what’s lagged—forces you to buy low and sell high, the very principle that underpins successful investing. More importantly, it keeps your portfolio in line with your risk tolerance and long-term plan. As discussed in Building a Portfolio You Can Sleep With, a portfolio that drifts too far from your intended allocation can lead to sleepless nights and rash decisions when markets turn volatile.

How Often Should You Rebalance?

There’s no one-size-fits-all answer. Some investors rebalance on a set schedule—quarterly, semi-annually, or annually. Others use thresholds, rebalancing only when an asset class drifts a certain percentage from its target. The key is consistency. Too frequent rebalancing can trigger unnecessary transaction costs and taxes, while waiting too long can let risks pile up. Your approach should reflect your investment strategy, portfolio size, and personal tolerance for risk and effort.

The Subtle Benefits Beyond Returns

While rebalancing is often discussed in the context of risk management, its benefits go deeper. By enforcing a systematic approach, you avoid the emotional pitfalls of chasing recent winners or abandoning laggards at the wrong time. This is particularly important in preventing overconcentration—something highlighted in The Danger of One “Hero” Stock, where a single outperforming holding can quietly dominate your portfolio and skew your risk profile.

Rebalancing can also help smooth out your investment journey, reducing the likelihood of large drawdowns. When paired with other long-term strategies—such as the Silent Power of Reinvested Dividends—rebalancing contributes to a steadier, more predictable compounding process over time.

Seeing the Drift: Tools and Tracking

Modern portfolio tracking tools make it easier than ever to monitor your allocation and spot when it’s time to rebalance. Paying attention to what Your Allocation Chart Is Trying to Tell You can reveal subtle shifts that might otherwise go unnoticed. Even if you’re managing small accounts, don’t underestimate the value of tracking and adjusting—Tracking Small Accounts Still Matters for building good habits and maintaining discipline.

Common Pitfalls to Avoid

- Letting emotions drive timing: Don’t wait for market headlines or gut feelings to dictate when you rebalance. Stick to your plan.

- Ignoring taxes and costs: Be mindful of transaction fees and potential capital gains, especially in taxable accounts. Sometimes, small drifts aren’t worth the cost of correcting immediately.

- Rebalancing too aggressively: Overzealous rebalancing can erode returns through unnecessary trades. Use reasonable thresholds or time-based rules.

The Quiet Power of Consistency

Rebalancing won’t make you rich overnight, nor will it shield you from every market downturn. But it is a quiet, steady force that keeps your investment plan on track, helping you avoid costly mistakes and stick with your long-term goals. In the end, the discipline of rebalancing is less about chasing returns and more about honoring the plan you set for yourself—one adjustment at a time.

For more on how asset allocation and risk management work together, see What “Portfolio Weight” Really Shows About Risk.